SOLVING THE STUDENT LOAN CRISIS IN AMERICA:

OLD DATA FROM 2019 & BEFORE: Update to come and all existing info to be revised on this page before the end of October 2022.

1: THE NUMBERS (Includes charts & graphs from ValuePenguin: https://www.valuepenguin.com/average-student-loan-debt

2: CURRENT STAFFORD BORROWING LIMITS & HISTORICAL INTEREST RATES (Data from studentaid.ed.gov)

3: FEDERAL SERVICES, PRIVATE STUDENT LOAN COMPANIES & CAPITAL ACCESS OPTIONS:

4: STUDENT LOAN ADVOCACY GROUPS, WATCH DOGS & REPORTS

5: CURRENT WAYS STUDENTS LOOSE FUNDING

6: SIMPLIFYING FAFSA FILING PROPOSED:

7: TUITION COMPARISON BY STATE: This will compare the cost of tuition in 50 different states plus US Territories for different programs.

8: TEMPORARY FEEL GOOD BUBBLE BEFORE THE STORM

9: COMPREHENSIVE MONLUX PLAN (PDF & WORD DOC) + IDEAS & INFO GRAPHIC SUMMARIES

1: THE NUMBERS:

(Graphs/Chart Data Sets from Value Penguin: Direct Access Link: https://www.valuepenguin.com/average-student-loan-debt )

STUDENT LOAN BORROWER AMOUNTS

STUDENT LOAN DEBT BY YEAR

AGE/YEAR OF STUDENT LOAN DEBT IN AMERICA

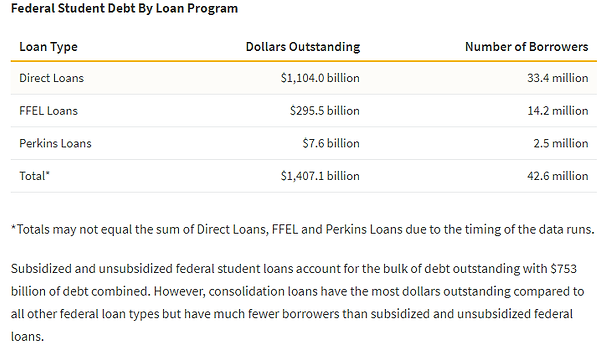

STUDENT DEBT BY PROGRAM

STUDENT DEBT BY STATE

*North Dakota excluded due to its reporting methods.

PRIVATE STUDENT LOAN DEBT

* Very Little Reporting was done prior to 2014 by Private Companies making it very difficult to accurately reflect the data let alone verify unless you have access to advanced mathematical software calculations in addition to insider confidential protected information data.

*In 2018 co signer requirements were increased for borrowers making it extremely difficult to obtain a private student loan without a cosigner further lowering capital access for students. A pendulum swing to the 2 edge sword. Most living wage of better jobs require a college degree. Most families don't cosign for students. Therefore the trap cycle begins of problem 1 with no capital access and problem of 2 of outrageous rates when one is lucky enough to get one.

GRADUATE V UNDERGRADUATE BORROWING

1ST YEAR PAID JOB INCOME V TOTAL STUDENT LOAN DEBT

*Asians actually did the best while African Americans did the worst and are still subject to discrimination in terms of both lending terms and pay. Hispanic women did better than white women whereas the white man did better than a Hispanic man.

* Due to lack of reporting data available at the time, Native Americans were not included in the published result.

ABOVE CHARTS, DATA SETS & GRAPHS FROM ValuePenguin: Direct Access Link: https://www.valuepenguin.com/average-student-loan-debt First viewed: October 2018. Accessed for use on this website: 1/5/2019 (January 5th, 2019)

2: CURRENT STAFFORD BORROWING LIMITS & HISTORICAL INTEREST RATES

Chart from studentaid.ed.gov ( https://studentaid.ed.gov/sa/types/loans/subsidized-unsubsidized ) Accessed January 5th, 2019

CURRENT STAFFORD STUDENT LOAN INTEREST RATES 7/1/2018-7/1/19:

Chart from studentaid.ed.gov ( https://studentaid.ed.gov/sa/types/loans/subsidized-unsubsidized ) Accessed January 5th, 2019 )

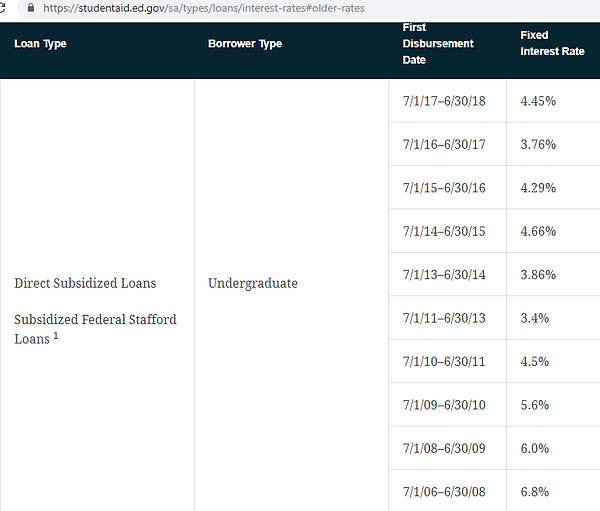

HISTORICAL STAFFORD INTEREST RATES:

UNDERGRADUATE: July 1st, 2006-June 30th, 2018

Chart from studentaid.ed.gov ( https://studentaid.ed.gov/sa/types/loans/interest-rates#older-rates ) Accessed: January 5th, 2019

GRADUATE/PROFESSIONAL JULY 1ST, 2006-JUNE 30TH, 2018

Chart from studentaid.ed.gov ( https://studentaid.ed.gov/sa/types/loans/interest-rates#older-rates ) Accessed: January 9th, 2019

3: FEDERAL SERVICES, PRIVATE STUDENT LOAN COMPANIES & CAPITAL ACCESS OPTIONS:

FEDERAL SERVICERS OF STUDENT LOANS

10 PRIVATE COMPANY BORROWING OPTIONS

DISCLAIMER: This information for the Federal Loan Servicers and Private Student Loan Companies was obtained on Wed January 9th, 2019. David Monlux is not responsible for changes in rates, company closures, new players, changes in policies/lending practices due to industry standards, economic changes and or changes in Federal/State laws/lending regulations before or after January 9th, 2019. Variable rates are always variable and can change at any time. This is meant to be a starting point. You the student or the cosigner borrowing are responsible for conducting your own research, reaching out to each company you are interested in and are responsible for any loan(s) you receive from said company. All of these company were found via independent research and no commission or benefits were obtained for recommendations. In addition no deal has been made for referral benefits either.

ADDITIONAL FUNDING OPTIONS

1: STATE LOANS & GRANTS: Varies by State. Please consult you state. Not every state has these programs and other may have them but you have to register by the end of your Freshman/Sophomore year of high school. Most students aren't even encouraged to begin looking at college until their Junior year.

2:EDUCATION SAVINGS ACCOUNTS & INVESTMENT PLANS: These normally take years to build and require advanced planning in addition to discretionary income to invest initially.

3: JOB: Assumed at 40 hours a week for all 52 weeks of the year below. Keep in mind that the average annual cost of school is over $20,000 a year and ALL earnings in the chart below are pre tax.

While the job method might sound appealing at first combined with financial aid here is why it is NOT as great as it sounds for a college/university student. First all of that money is pre tax. Second it is hard to maintain regular hours due to class offerings varying every semester while most employers are neither flexible or accommodating. Third is that under federal aid rules, once you start making above x amount you can get kicked off federal aids and loan. In addition research and papers take time outside of the classroom. Its possible that a student can make the money financially working full time but in doing so their classroom studies suffer or they get no sleep (serious health problem) between work, class and all the assignment loads. If you don't believe that long papers are assigned just go to https://www.davidmonlux.com/works and look at 2: Cuba Human Rights paper, 3: MSS China Simplified, 7 Intl Terror Paper, 8 Peru Operation Car Wash & 10 Catty Wampis. In addition many students are victims of anxiety attacks from financial issues. In addition when colleges list the average cost of attendance ($23,740 per year) this only includes the basic meal plans, dorm, fees and tuition. This excludes textbooks, parking, transportation, family obligations and additional meals (most meal plans only cover 2 meals a day for 6 days a week leaving 9 meals not included) NOT covered. Between being disqualified for loans, only being able to go part time work, choosing between a degree or work instead of both and no sleep causing serious health issues, there is a strong incentive NOT to work and a huge disincentive to work. Until this issue combined with the funding is addressed, the status quo will NOT change. We have entered the cycle of insanity of doing the same old thing as we did last week without a new thing to do (That 70's Show) but repeat and more failure keeps happening while expectations for success go up. Its time to come up with a new system that prioritizes student health, creates incentives to work and gets students the capital funding access with dignity that they need to complete their degrees. Its time to put the dignity back into work, common sense into college funding and remove the serious mental health exhaustion obstacles facing students today.

4: UNIVERSITY INSTITUTIONAL LOANS & SCHOLARSHIPS: Very hard to obtain. Most make any student below a 3.00 GPA ineligible. Deans & Departments do play favorites, are underfunded by the State/Federal government and retention standards are set that most students loose the funding within 1-2 semesters.

5: INSTALLMENT & PERSONAL LOANS: Variable in obtaining. Be careful not to fall victim to predatory lenders.

6: PRESIDENTIAL PARDON: The US President has the power to forgive any and all debts to the United States. Stafford Loans are federal loan debt to the federal government, therefore as a federal debt, the President has the power to pardon any and all STAFFORD Loans. I therefore call upon the US President with the stroke of the pen using the pardon power to pardon part or all of existing student Stafford loans.

7: PAID OFF GAME SHOW: More info to come soon.

8: ANONYMOUS RICH PERSON: Every college student dream. Rarely happens and is a terrible plan to rely on.

9: SPECIAL LEGAL PROGRAMS & FEDERAL GOVERNMENT FORGIVENESS PROGRAMS: Comprehensive Plan coming soon.

10: DIVINE INTERVENTION: Student Financial Aid Prayer:

Financial Aid full of Grace OR NOT with thee? Blessed are thou among thy grant and loan disbursements. Financial Aid, Gate Keeper of Funds, will thou release mana from heavenly federal coffers that is aid OR send me to my academic and financial death? AMEN

If this isn't said around disbursement every semester, than it should be.

4: STUDENT LOAN ADVOCACY GROUPS, WATCHDOGS & REPORTS:

ADVOCACY GROUPS/WATCH DOGS

MAJOR REPORTS & POLICY BRIEFS

(Different reports may obtain different opinions, ideas, causes and or solutions to student loan issues. Each report is public record and sole authorship/ownership belongs to said group/organization/individual. As part of public research David is attempting to provide access to multiple public reports all in one place. There are many additional private reports that Monlux has had the privilege to view and access, however due to the nature of those reports he is prevented from publishing them here or providing links as they were done for major student loan companies or by private enterprises and banks. He will not reveal his contacts and is forever grateful for that insightful information. However everything proposed on this site only deals with information from the official public record and reports).

AMERICAN STUDENT ASSISTANCE REPORTS

These are just 4 of the many reports on student financial issues by the American Student Assistance (ASA). To see more reports by the fabulous hardworking and dedicated organization head over to their website at https://www.asa.org/

COLLEGE COST (LUMINA FOUNDATION)

These are just two (2) of the many important and high profile student reports done by the College Cost portion of the Lumina Foundation. To see more of their research and data head over to https://www.luminafoundation.org/resources/college-costs-in-context

INSTITUTE FOR COLLEGE ACCESS & SUCCESS

These are just a small recent sample of policy briefs and reports done by the Institute for College Access and Success. To see the long list of all of their reports, briefs and publications please head to https://ticas.org/publications

5: WAYS STUDENTS LOOSE FUNDING FORCING THEM TO DROP OUT

6: PROPOSED SIMPLIFYING FAFSA FILING FOR STUDENTS

7: TUITION COMPARISON BY THE 50 US STATES & TERRITORIES

50 US STATES

ALABAMA

ALASKA

ARIZONA

ARKANSAS

CALIFORNIA

COLORADO